The 23-Day Gap

A typical UK ADC loan operates on three different cycles:

The cadence mismatch

A typical UK ADC loan operates on three different cycles:

- Drawdowns are requested on stage completion, typically every 6-10 weeks, and approved within 5-10 working days of QS cost certification

- QS site visits happen every 90 days (quarterly), or every 60 days for higher-risk projects

- Covenant reviews happen quarterly, tied to QS reports

From 1 January 2027, Basel 3.1 adds a fourth cycle:

- PRA monitoring expectation (PS1/26) is continuous

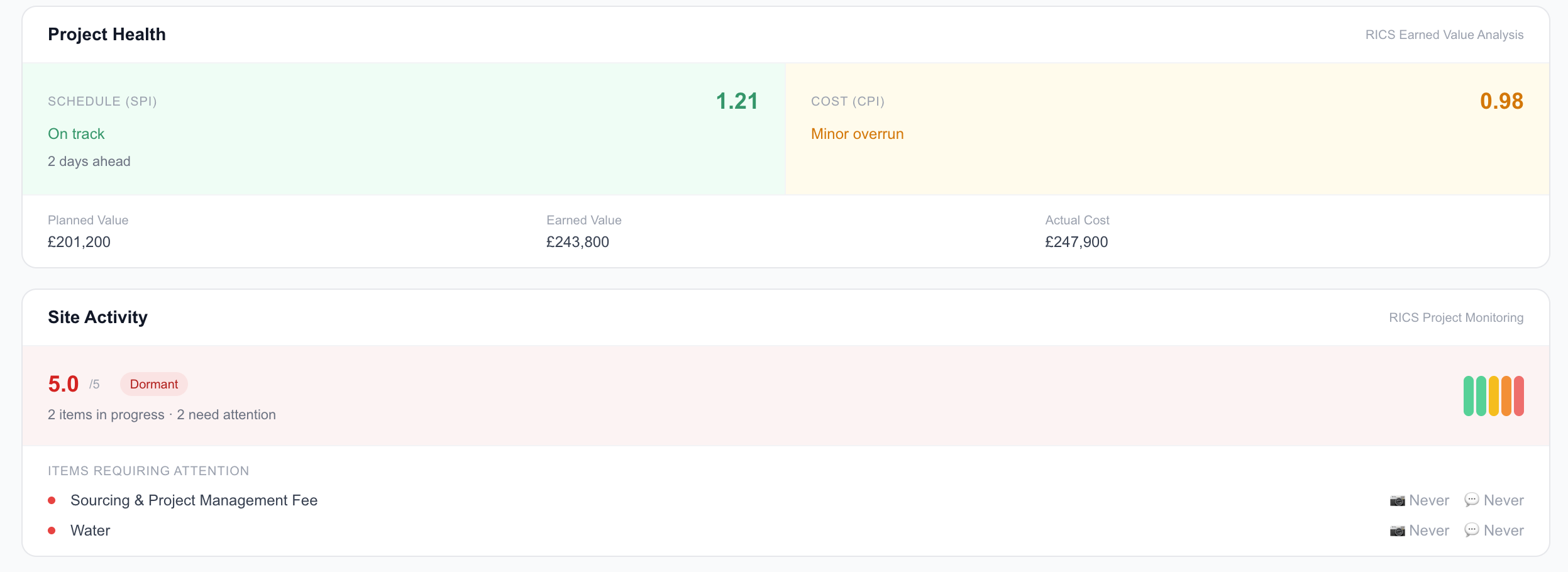

The gap between "quarterly QS visits" and "continuous monitoring" is where most lenders will fail the standard. Not because their QS is bad, but because the operating model wasn't designed for real-time visibility.

The PRA doesn't require daily reports. "Continuous monitoring" means the lender should be able to answer, at any point in the loan lifecycle, whether covenants are being met and whether the project is on track. That's a data availability question, not a labour question.

The 23-day blind spot

Here's what happens in the gap between QS visits:

The problem. Between Day 1 and Day 90, the lender had no visibility into where drawdown funds were actually going. By the time the QS sees it, the spend has already happened, the variance is historical, and the only question is how to classify it (not whether to prevent it).

This is the 23-day gap. It's not 90 days (full cycle), because most lenders review the QS report within a week of receiving it. The real blind spot is the period between when money moves and when the next QS report closes. For a quarterly cycle, the average gap is 23 days. For a 60-day cycle, it's 16 days.

PS1/26 requires lenders to know, continuously, whether covenants are being met. A 23-day lag means you're always managing breaches in arrears.

Three blind spots the current model creates

1. Drawdown misuse (spend doesn't match the approved line item)

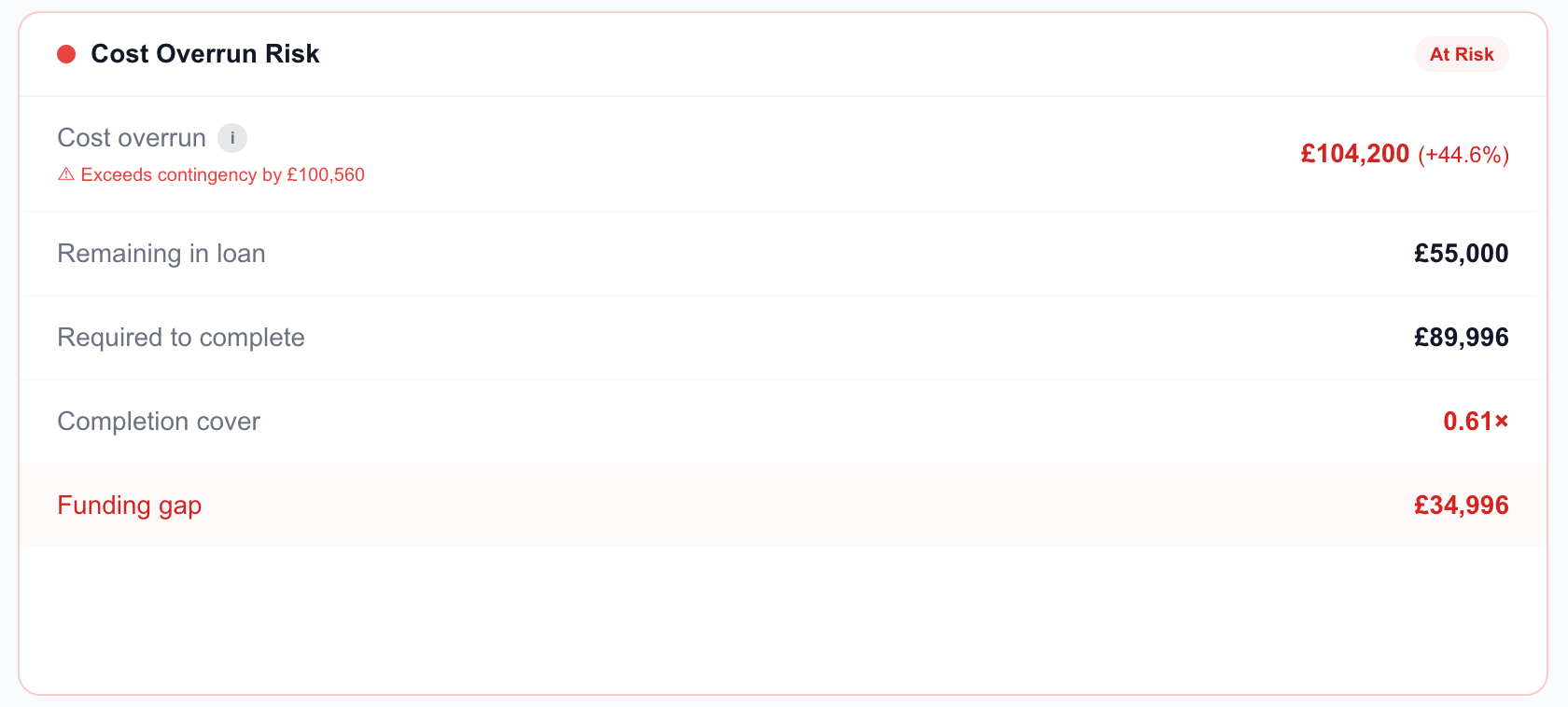

You approve £400k for groundworks. £140k of it pays a supplier who's not in the contract. The borrower isn't committing fraud. They're covering a cost overrun from an earlier stage that they didn't disclose. The cost plan is now wrong, your LTV assumption is wrong, and if the overrun pushed LTV above the Article 124K threshold, you've been reporting the wrong risk weight to the PRA for 23 days without knowing it.

2. Programme slippage hidden until too late

A project falls 11 days behind between QS visits. The borrower doesn't report it. The QS sees it 79 days later. By then the delay in groundworks has pushed back the frame, delayed weatherproofing, and the project can no longer complete before the facility expires. At Day 79, your options are refinance, write-off, or enforcement. At Day 11, you had three others.

3. Covenant breaches surfacing in arrears

Your facility agreement has a 75% LTV covenant. Between QS visits, the borrower withdraws £80k from the SPV to cover cashflow elsewhere. Equity drops from £500k to £420k. LTV moves from 75% to 79%. You're in breach. You won't know until the next QS report reconciles investor vs lender funds. By then the breach has been live for 23 days and you've already approved another drawdown based on a compliance position that was no longer true. That's the Pillar 2 exposure: a breach running undetected while the lender continues to advance funds.

What continuous monitoring actually means operationally

The PRA isn't asking lenders to send a QS to site every week. Continuous monitoring means having the infrastructure to detect breaches as they happen, not as they're reported. Three shifts close the gap.

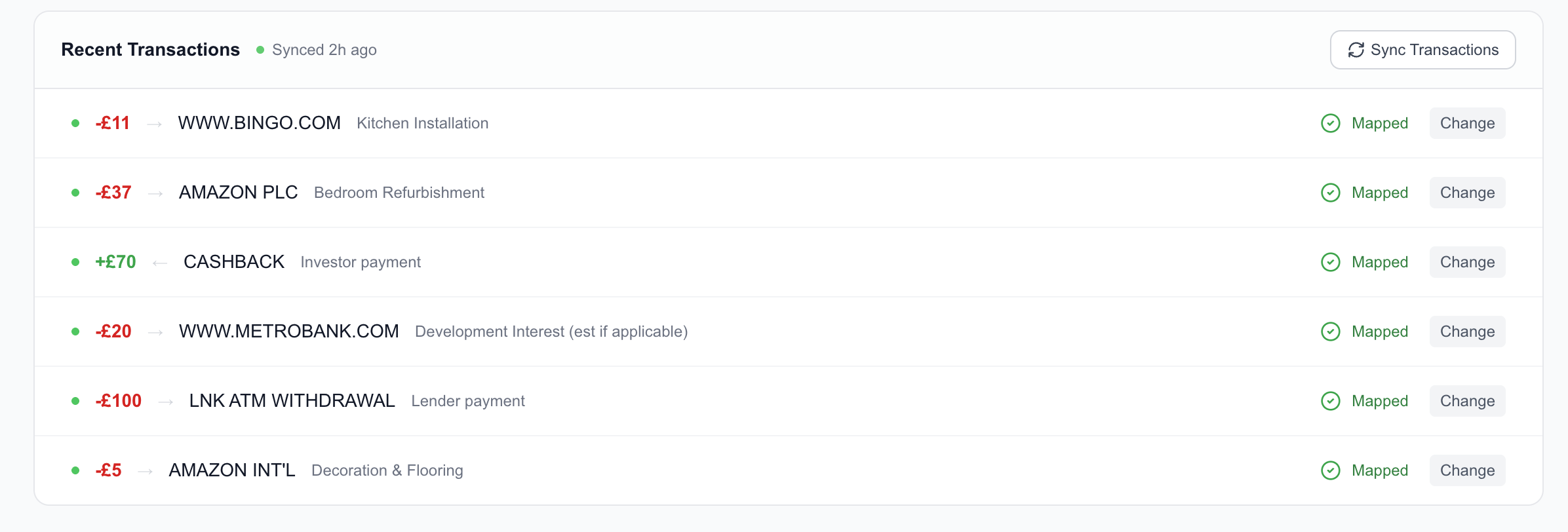

1. Bank-feed visibility on the borrower SPV

Connect to the borrower's project bank account via open banking. Every transaction flows in real time: investor deposits, lender drawdowns, contractor payments, supplier payments, equity withdrawals. If £140k moves to an unknown supplier on Day 14, you see it on Day 14, not Day 90.

2. Drawdown-to-spend visibility

Depending on the lender, drawdowns are either advanced for the next stage on QS certification of the previous one, or released in arrears once costs have been incurred. Either way, funds land in the borrower's SPV and the developer controls where they go from there. That's where visibility typically ends.

The bank feed changes that. Every outflow from the SPV is visible as it happens. The credit officer can see whether spend is tracking against the certified cost plan, or whether funds approved for one stage are being used to cover costs from another. The system shows where money is going. The lender decides what to do about it.

3. Programme and cost in one view

A cost overrun that looks small and a programme delay that looks small can each appear manageable on their own. Together, at the same time, they indicate a contractor spending more and delivering less. That's a credit decision point. Continuous monitoring means you see both signals together, not two months apart.

Case study: the £140k drawdown scenario

Let's walk through how continuous monitoring changes the outcome in the timeline above.

| Day | What happens (traditional model) | What happens (continuous monitoring) |

|---|---|---|

| Day 1 | QS completes site visit. All green. | Same. But the lender now has live bank-feed connection to the SPV. |

| Day 7 | Lender approves £400k for groundworks (ABC Groundworks Ltd). | Same. System logs the drawdown: £400k against the groundworks line item in the certified cost plan. |

| Day 9 | Funds hit the SPV. | Bank feed shows the drawdown landing in the SPV. Same. |

| Day 14 | £140k leaves the SPV to XYZ Supplies (not in the contract). No one sees this yet. | Bank feed shows £140k leaving the SPV to XYZ Supplies. The drawdown was certified against groundworks costs. The credit officer can see this outflow immediately and call the borrower to understand what it relates to. They have a choice: accept the explanation, or pause further drawdowns until the QS re-validates the cost plan. |

| Day 23 | Another £80k is reallocated. Still no visibility. | Second alert. Credit officer requests a quick QS cost reconciliation call (not a full site visit). QS confirms the overrun is real but contained. Decision: allow the £80k reallocation, but no further drawdowns until the next full QS visit. |

| Day 90 | QS visit surfaces the £220k variance. Too late to intervene. Money is spent. | QS visit confirms what the lender already knows. No surprises. Credit officer has already made the containment decision 67 days earlier. |

Outcome. In the traditional model, the lender discovers the problem at Day 90, when the QS reconciles retrospectively. In the continuous model, they see the outflow on Day 14, the day it happens, when they can still act on it.

The credit officer doesn't watch every transaction. During the weekly exception review, they open the dashboard and see that a £140k outflow to XYZ Supplies doesn't match the approved drawdown for ABC Groundworks Ltd. They call the borrower, log the explanation, and decide whether to allow it or pause further drawdowns. Total time is 15-30 minutes across the whole portfolio. That's continuous monitoring: exception-driven, not labour-intensive.

Implementation checklist

What a lender needs to implement continuous monitoring without doubling headcount:

1. Infrastructure

- Open banking connection to every borrower SPV (via FCA-regulated provider)

- Transaction classification engine (investor vs lender vs contractor vs supplier)

- Drawdown approval log (amount, line item, expected payee, date)

- Reconciliation engine (match outflows to approved drawdowns)

- Alert system (flag unmatched transactions, threshold breaches, programme variances)

2. Policy

- Define "material variance" threshold (e.g., any single outflow >10% of approved drawdown to a non-approved payee)

- Set alert routing rules (who gets notified, how fast)

- Document escalation process (alert → call borrower → decide: approve reallocation / freeze drawdowns / request mini-review)

- Update facility agreements to require open banking consent (or make it a condition precedent for first drawdown)

3. Process

- Weekly exception review (credit officer reviews flagged transactions, 15-30 mins per portfolio)

- Monthly covenant dashboard (automated: LTV, equity %, ICR, programme status, no manual calc needed)

- Quarterly QS validation (QS report confirms what the lender already knows from live data)

4. Evidence (for PRA SREP)

- Audit trail: every flagged transaction, every borrower call, every decision logged

- Dashboard screenshots: monthly covenant status as of each month-end

- Exception log: all variances >threshold, with resolution notes

- Policy document: how continuous monitoring is implemented, who is responsible, what the thresholds are

What this doesn't replace

Continuous monitoring is not a substitute for:

- QS site visits. The QS validates physical progress, quality of work, and programme realism. You can't automate that. But you can reduce the frequency of visits if you have real-time financial visibility.

- Credit judgement. The system flags exceptions. The credit officer decides what to do about them. A £140k variance might be fine (approved reallocation). Or it might be the first sign of borrower distress. The data gives you the option to intervene. It doesn't make the decision for you.

- Legal documentation. Facility agreements still need LTV covenants, equity maintenance clauses, drawdown conditions. Continuous monitoring helps you enforce them. It doesn't replace them.

We're not saying quarterly QS visits are bad. We're saying the gap between visits is where breaches go undetected. The QS tells you what happened. Continuous monitoring tells you what's happening. You need both.

Regulatory context: what PS1/26 actually says

The PRA's Policy Statement PS1/26 (Basel 3.1 implementation) sets out the prudential treatment for ADC exposures under Article 124K. The headline is the 100% vs 150% risk weight, but buried in the conditions is this:

"Firms must apply prudent underwriting standards and maintain continuous monitoring of the exposure, including the financial condition of the borrower and the value of the collateral."

SS3/24, paragraph 2.15

The phrase "continuous monitoring" appears 6 times in SS3/24. It's not optional. It's not "best practice." It's a condition of claiming the 100% risk weight.

The PRA doesn't define what "continuous" means in operational terms. That's deliberate. It allows firms to design systems that fit their book. But the expectation is clear: you should know, at any point, whether covenants are being met. A quarterly QS review doesn't meet that standard.

Summary

- Most UK development lenders fund monthly and review quarterly. PS1/26 expects continuous monitoring. The average gap is 23 days.

- In that gap, three things go undetected: drawdown misuse, programme slippage, and covenant breaches.

- Closing the gap requires three operational shifts: bank-feed visibility on the borrower SPV, drawdown-to-spend visibility so the lender can see where funds actually go, and programme and cost data in a single view.

- Implementation requires infrastructure (bank feeds, classification, alerts), policy (thresholds, escalation), and process (weekly exception review, monthly covenant dashboard). It does not require more QS visits or more headcount.

- The risk weight consequence is real: a covenant breach running undetected while the lender advances funds is evidence of inadequate monitoring under PS1/26. That is a Pillar 2 charge risk.

- The QS validates physical progress. Continuous monitoring validates financial compliance. You need both.

The 23-day gap is fixable. The question is whether lenders will close it before the PRA starts asking why they haven't.

Close the gap

Mintstone gives UK development lenders the infrastructure to monitor ADC exposures continuously without doubling headcount or QS budgets.

See how it works →