The Article 124K Eligibility Problem

The risk weight is a snapshot, not a guarantee

Under Basel 3.1 PS1/26, most ADC exposures carry a 150% risk weight. Article 124K provides an exception: exposures that meet a defined set of conditions may be held at 100%. That 50 percentage point difference has a material impact on the capital a lender must hold against each facility.

The conditions are assessed at origination. The credit paper confirms them. The risk weight is set at 100%. And then the loan runs for 12 to 18 months during which those conditions are, in most cases, not monitored systematically.

On a £2m ADC exposure, the difference between 100% and 150% risk weight is £1m of additional risk-weighted assets. At an 8% capital requirement, that is £80,000 of additional capital that should be held against that one facility. A lender with 20 facilities that have silently lost 124K eligibility has a meaningful capital adequacy gap relative to what the SREP review will find.

Which conditions can fail mid-loan

Not all Article 124K conditions require ongoing monitoring. The ones that do fall into three categories:

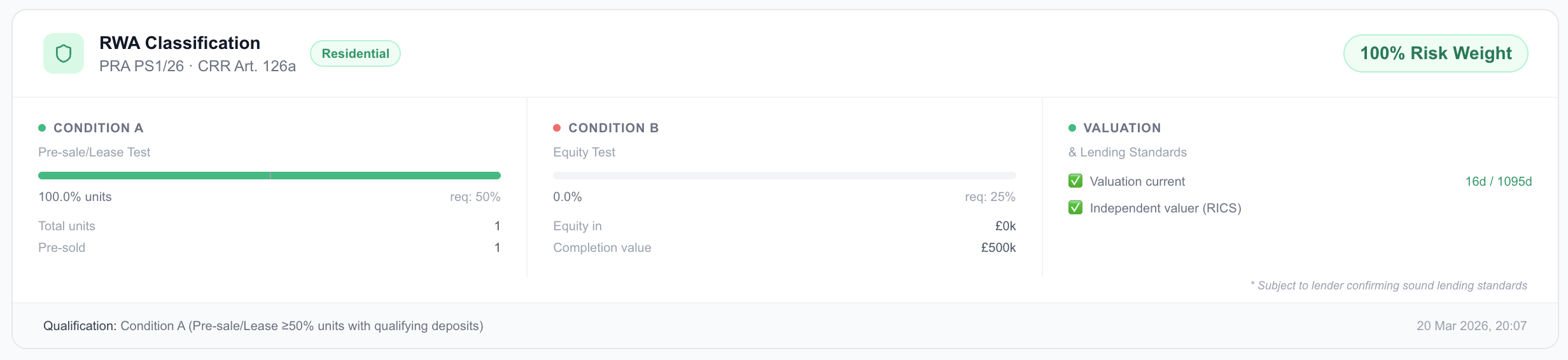

1. LTGDV threshold

Article 124K sets a maximum loan-to-GDV for residential ADC exposures to qualify for the 100% risk weight. GDV is set at origination. If market conditions deteriorate during the loan, the real LTGDV against the current market value of the completed units rises even though the loan balance hasn't changed. If that drift pushes the real LTGDV above the Article 124K threshold, the eligibility condition is no longer satisfied.

This is not a theoretical risk. Residential markets move. A development with an 18-month build programme that started in a strong market may reach completion in a weaker one. The GDV assumption used to calculate LTGDV at origination may be 8 to 12% above what the units will actually sell for. The eligibility threshold is calculated against the origination GDV. The real position is calculated against the current market.

2. Borrower equity position

Some Article 124K interpretations and lender credit policies require the borrower to have contributed a meaningful equity stake relative to total development costs. That equity is contributed at or before first drawdown. It is not replenished automatically if costs overrun.

If a project runs materially over budget, the developer's equity as a percentage of total costs erodes. At origination, equity might represent 25% of the project. After a 15% cost overrun funded from additional borrowing or contingency, that percentage is meaningfully lower. Whether this technically breaks an Article 124K condition depends on how the condition is framed in the facility agreement and credit policy, but it is a monitoring question that most lenders are not asking during the loan.

3. Pre-sale and pre-let requirements

Some Article 124K-eligible structures require a minimum level of pre-sales or pre-lets to qualify. A development where 30% of units are pre-sold at origination qualifies. If a buyer pulls out mid-build and that pre-sale falls away, the qualifying percentage drops. If it drops below the threshold, the eligibility condition fails.

Pre-sale agreements can fall through. Buyers can exercise cooling-off rights, fail to complete on mortgage, or withdraw during the build. Each withdrawal is a discrete event. None of them automatically notifies the lender in a way that triggers a risk weight review. The credit paper says "30% pre-sold." The live position may be 18%.

4. Sunset clause and long-stop expiry

Some 124K-eligible structures have time conditions: the development must complete by a certain date for the favourable risk weight to apply. If the programme slips and the long-stop date is missed, the condition fails. The exposure should be reclassified.

Programme slippage in UK development finance is common. A 10 to 15% time overrun on a 12-month programme means the facility runs into month 13 or 14. If the Article 124K conditions were structured with a completion deadline that corresponds to the original programme, slippage puts that condition at risk.

The reclassification is per exposure, not portfolio-wide

The capital impact of failing to monitor 124K eligibility is not binary. It accumulates exposure by exposure. Five facilities that have quietly lost 124K eligibility add five incremental RWA increases to the book. Under a SREP review, the PRA will look at whether each exposure is correctly classified and whether the lender has evidence that the conditions were monitored throughout the loan lifecycle, not just at origination.

| Condition at risk | What causes it to fail mid-loan | RWA consequence |

|---|---|---|

| LTGDV threshold | GDV drift from market softening during the build period | Exposure reclassified from 100% to 150% risk weight on the full loan balance |

| Borrower equity percentage | Cost overruns that reduce equity as a proportion of total development cost | Eligibility condition may fail depending on facility agreement wording; risk weight review required |

| Pre-sale requirement | Buyer withdrawal reducing pre-sold percentage below qualifying threshold | Condition fails; exposure reclassified at 150% until pre-sale position is restored |

| Long-stop / sunset clause | Programme slippage causing completion after the condition deadline | Time condition fails; reclassification required from breach date |

| Commercial element | Mixed-use development where commercial portion is assessed separately; 124K does not apply to commercial ADC | Commercial sub-exposure always at 150%; residential sub-exposure assessed on its own conditions |

What continuous eligibility monitoring looks like

Monitoring 124K eligibility continuously does not mean re-underwriting every loan every month. It means tracking the specific conditions that can change, and flagging when they approach or breach the threshold that would require reclassification.

LTGDV monitoring

Land Registry comparable sales data, refreshed as new transactions are registered, gives a live picture of where the local market is relative to the GDV at origination. Applying a market adjustment factor to the origination GDV gives a continuously updated LTGDV figure. When that figure approaches the Article 124K threshold, the lender has advance notice that a formal revaluation may be needed before the condition fails.

Equity position monitoring

Cost overruns are tracked through the drawdown process and QS certifications. When the total projected cost of a development increases materially relative to the origination cost plan, the borrower's equity as a percentage of total development cost changes. That calculation can be maintained continuously from cost tracking data without requiring a new credit paper.

Pre-sale status tracking

Pre-sale agreements are logged at origination. The lender should track whether those agreements remain in place. A simple register of pre-sale status, updated when the borrower reports changes, gives a live picture of whether the qualifying percentage is being maintained. This is an information requirement on the borrower, not a monitoring burden on the lender.

Programme and long-stop monitoring

If a time condition exists, programme slippage monitoring feeds directly into eligibility monitoring. A project running at SPI 0.8 from month four is already on a trajectory that may breach a long-stop tied to the original programme. Seeing that trajectory early means the lender can either restructure the time condition before it fails, or price the reclassification risk into any extension decision.

The SREP evidence question

The PRA's SREP review will look at whether the risk weights assigned to ADC exposures are correct and whether the lender can demonstrate that eligibility conditions were monitored throughout the loan lifecycle. A credit paper that confirms 124K eligibility at origination but provides no evidence of ongoing monitoring is not a satisfactory answer to that question.

The evidence standard is not onerous. It requires a record of what conditions were being tracked, how frequently, what the status was at each review point, and what action was taken when conditions were at risk. That is an audit trail question, not a deep analysis question. But it requires that someone was actually watching the conditions, not just ticking them at origination and moving on.

Summary

- Article 124K eligibility is conditional throughout the life of the loan, not just at origination. Several conditions can fail mid-loan without any formal notification to the lender.

- The conditions most at risk during the loan are: LTGDV threshold (market drift), borrower equity percentage (cost overrun), pre-sale requirement (buyer withdrawal), and long-stop clauses (programme slippage).

- Reclassification happens per exposure. Each facility that flips from 100% to 150% adds a discrete RWA increase. A book with several quietly reclassified exposures has a cumulative capital adequacy gap.

- For mixed-use developments, the residential and commercial portions are assessed separately. The commercial portion is always at 150%. The residential portion is assessed on its own 124K conditions.

- Continuous eligibility monitoring does not require re-underwriting. It requires tracking the specific conditions that can change, flagging when they approach the threshold, and maintaining an audit trail for SREP evidence.

Monitor 124K eligibility across your portfolio

Mintstone tracks the Article 124K conditions that can change during the loan lifecycle. LTGDV updates as market data moves. Cost overrun feeds into equity position. Pre-sale status and programme slippage are monitored continuously. The audit trail is built automatically.

See how it works →