The Contractor Blind Spot

A typical UK development finance credit paper will describe the borrower in detail. Developer experience, track record of completed schemes, GDV delivered, net worth, personal guarantee. It will note the planning status, the exit strategy, the comparable sales evidence. It is a thorough assessment of the developer.

What the credit paper says

A typical UK development finance credit paper will describe the borrower in detail. Developer experience, track record of completed schemes, GDV delivered, net worth, personal guarantee. It will note the planning status, the exit strategy, the comparable sales evidence. It is a thorough assessment of the developer.

On the contractor, it will usually say something like this:

"The development will be undertaken by [Contractor Name], an experienced regional contractor with a strong track record of residential delivery."

That sentence is almost always the full extent of contractor assessment in the credit paper. No overrun history. No current workload. No view of how that contractor has performed on other lenders' books. No check on whether they are currently running six other sites simultaneously.

The developer signs the facility agreement. The contractor builds the project. Those are different people. The credit paper assesses one of them.

Why this matters more than it appears

If the developer runs into trouble, the lender has recourse: personal guarantee, asset charge, SPV control. The facility agreement is designed around developer risk.

If the contractor runs into trouble, the lender has almost none of that. The contractor isn't a party to the facility agreement. There is no personal guarantee from the builder. The lender's direct exposure to contractor failure is indirect: programme slippage, cost overruns, potential insolvency mid-build.

Three scenarios where contractor risk materialises in ways the credit paper couldn't predict:

1. The overextended contractor

A contractor takes on more sites than they can resource. Each one individually looks fine at origination. Across six lenders' books simultaneously, the contractor is running 14 active sites with a team that can realistically manage eight. Programme slippage starts at the newest sites first, because that's where management attention is thinnest. No single lender knows about the other 13 sites.

2. The historically slow contractor

A contractor has a consistent pattern of finishing 12-15% late across their project history. On a 9-month programme, that's a 5-6 week overrun on average. The credit paper says "strong track record." The long-stop date in the facility agreement assumes the stated programme. The lender is pricing a loan that will, based on this contractor's actual behaviour, require a 4-6 week extension before work has started.

3. The contractor who consistently overbills

Some contractors have a consistent pattern of submitting drawdown requests above the QS-certified amount. On any single project it looks like a rounding issue or an admin lag. Across ten projects, it's a billing pattern. The lender who only sees one project in their book never spots it. The lender with cross-portfolio visibility sees the contractor's average overbilling rate and can price that into how tightly they require QS sign-off before releasing funds.

Why lenders don't assess contractors properly

This isn't carelessness. It's a structural data problem.

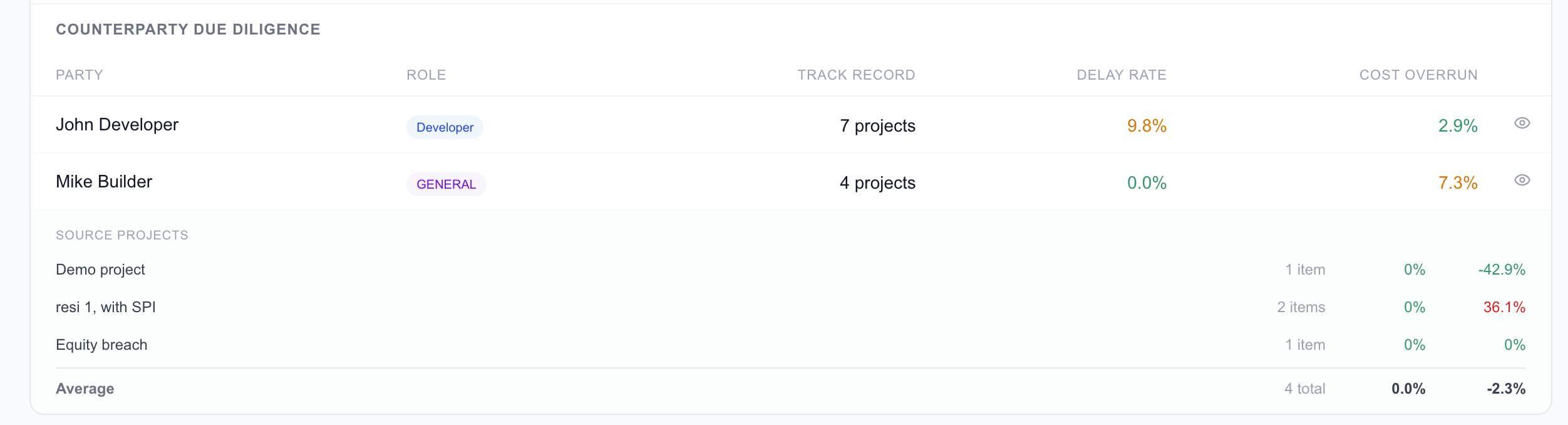

Each lender only sees their own loans. A contractor who has delivered cleanly for one lender may be overextended across three others simultaneously, and no single lender would know. There is no shared registry of contractor performance. No equivalent of a credit bureau for construction execution. The QS who visits the site has typically never worked with this contractor before on this lender's behalf, and has no access to how that contractor performed on their other projects.

The result is that "reputable contractor" in a credit paper means: we couldn't find anything bad about them in our own portfolio, and the QS didn't raise any concerns at site visit one. That's a very low bar for someone who is about to build a £2m scheme your capital is funding.

Consumer lenders solved this problem 30 years ago. Before credit bureaus, each lender only saw their own customer's repayment history. A borrower could default with one lender and get a new loan from another the same week. Credit bureaus aggregated cross-lender data. Development finance hasn't had an equivalent for contractor execution risk. Every lender is still making decisions based only on what they've seen themselves.

What contractor data actually tells you

The data point that matters most is average programme overrun across all completed projects. Not the developer's reference. Not the QS's initial impression. The actual percentage by which this contractor's projects have finished late, averaged across their full portfolio history.

That number, applied to the stated programme, gives you a more honest predicted completion date than any optimistic programme the contractor submits at origination.

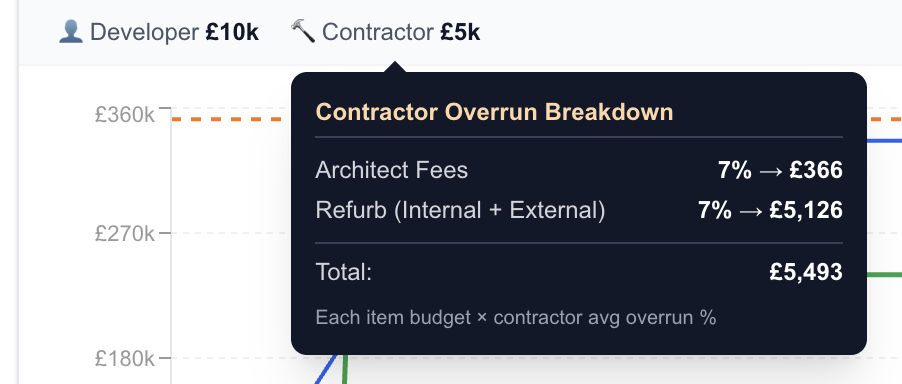

The second data point is billing accuracy: how closely this contractor's drawdown requests have tracked QS-certified amounts across their project history. A contractor who consistently submits requests above certification isn't necessarily fraudulent, but it creates friction, delays, and in some cases inflated cost plans. Knowing the pattern before origination lets the lender set appropriate release conditions from the start.

| Contractor history | Stated programme | Statistically likely duration | Long-stop risk |

|---|---|---|---|

| 5% average overrun | 9 months | 9.5 months | Low, manageable with standard buffer |

| 12% average overrun | 9 months | 10.1 months | Moderate, long-stop needs to reflect this |

| 20% average overrun | 9 months | 10.8 months | High, likely to breach a standard 12-month long-stop |

| First project on record | 9 months | Unknown | Wider confidence interval, price accordingly |

The second useful data point is concurrent workload. A contractor running three active sites has a meaningfully different risk profile than the same contractor running twelve. That's not a judgement about their quality. It's a capacity question. A contractor with finite management bandwidth spread across too many sites will deprioritise the ones where the lender is least likely to escalate quickly. New relationships are often lowest priority.

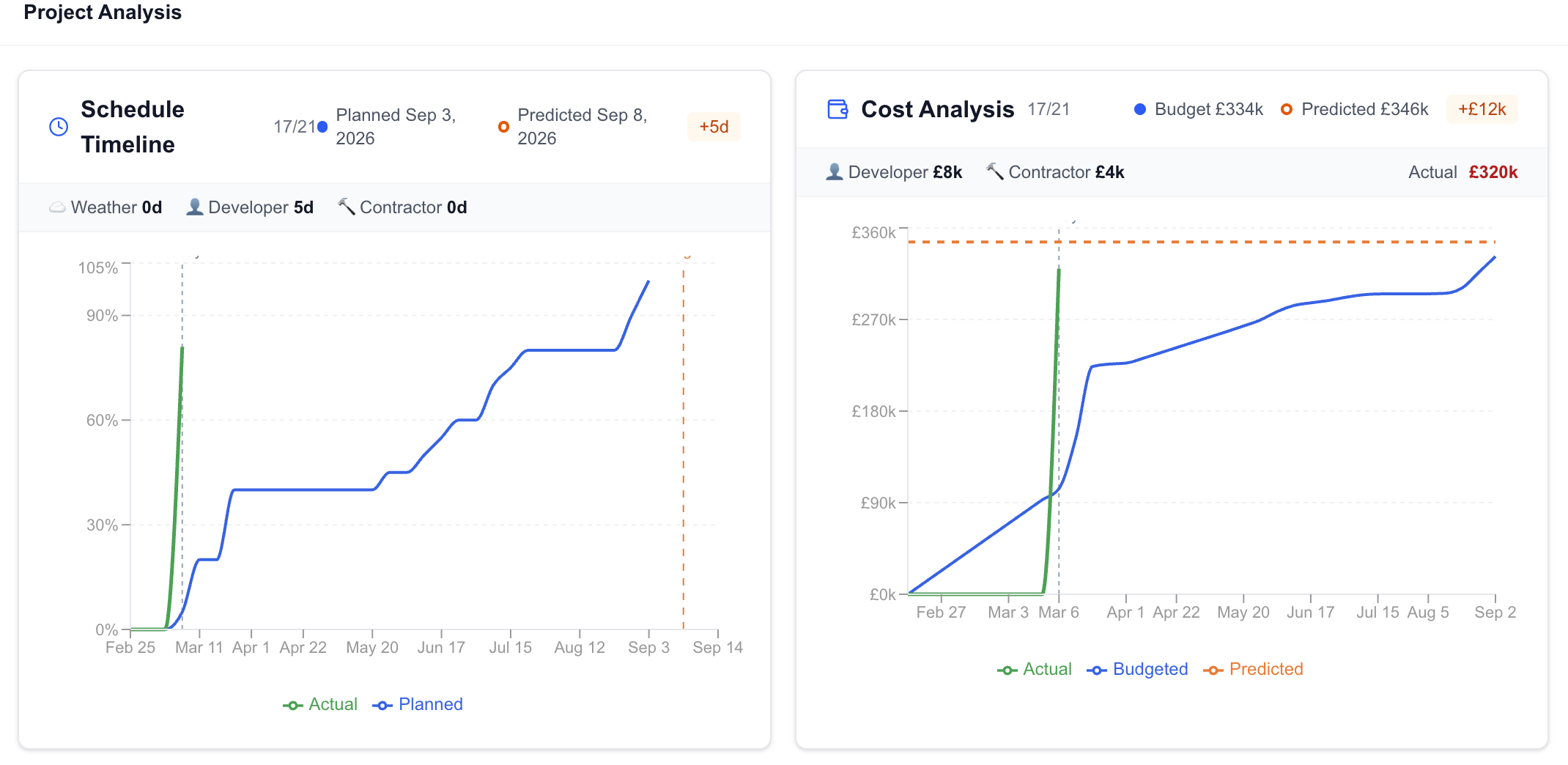

The three-line S-curve and what it shows

When contractor history is available, a predicted completion curve can be built at origination, before the first drawdown, based entirely on data from outside the current project.

The chart shows three lines:

- Planned: the programme the contractor submitted at origination, fixed

- Actual: what has been completed to date, updated as confirmed work items come in

- Predicted: where this project will most likely finish, based on this contractor's average overrun history, this developer's variation patterns, and weather data for the location and stage. Current project events do not move this line.

The gap between the planned and predicted lines at origination is the honest long-stop risk. If that gap already overlaps the facility's long-stop date, the lender has a structural problem to price before a single brick is laid.

As the build progresses, the actual line confirms or challenges the prediction. A contractor running ahead of their historical pattern is a positive signal. A contractor tracking exactly at their historical overrun rate is behaving as expected. A contractor running significantly worse than their own history is a new signal that something has changed on this project specifically.

What this means at origination vs during the loan

At origination

Contractor history changes two things in the credit decision:

- Long-stop date: Set it based on the statistically likely completion, not the optimistic programme. A contractor with a 15% average overrun on a 9-month build should have a long-stop at 11-12 months minimum, not 10.

- Risk pricing: A contractor with a consistent overrun history is a quantifiable risk. It can be priced into the arrangement fee, the margin, or the extension fee schedule. Currently it isn't priced at all, because it isn't measured.

During the loan

Cross-portfolio contractor monitoring means the lender gets an early signal when the same contractor starts underperforming on another active project. If the contractor is running at SPI 0.7 on a different scheme in the portfolio, that's a leading indicator for every other project they're running simultaneously, including yours.

What the credit paper should say instead

The sentence "experienced regional contractor with a strong track record" should be replaced with something like this:

"[Contractor Name] has completed 18 residential schemes over the past four years. Average programme overrun across completed projects: 8%. Current active sites: 4. Based on historical overrun, the predicted completion range for this scheme is [X] to [Y] months against a stated programme of [Z] months. Long-stop date has been set at [date] to reflect the upper end of this range."

That requires data. Most lenders don't have it because they've never collected it systematically. The ones who start collecting it now will be pricing contractor risk explicitly while competitors are still pricing it at zero.

Summary

- Credit papers assess the developer thoroughly and the contractor minimally. The contractor builds the project.

- The structural reason is data: each lender only sees their own portfolio. There is no cross-lender view of contractor execution history.

- The key data points are average programme overrun across all completed projects, and concurrent active workload at origination.

- Contractor history changes two things: the long-stop date (set it honestly) and risk pricing (price what you can now measure).

- During the loan, cross-portfolio contractor monitoring means underperformance on one project is a leading indicator for all projects that contractor is running simultaneously.

The contractor blind spot isn't a compliance question. It's a credit quality question. Lenders who measure it will make better decisions. Lenders who don't will keep discovering contractor risk at month eight, when the options have narrowed considerably.

See contractor data across your portfolio

Mintstone tracks contractor performance across all active and completed projects on the platform. The cross-portfolio view is available from day one of the first loan.

See how it works →